88

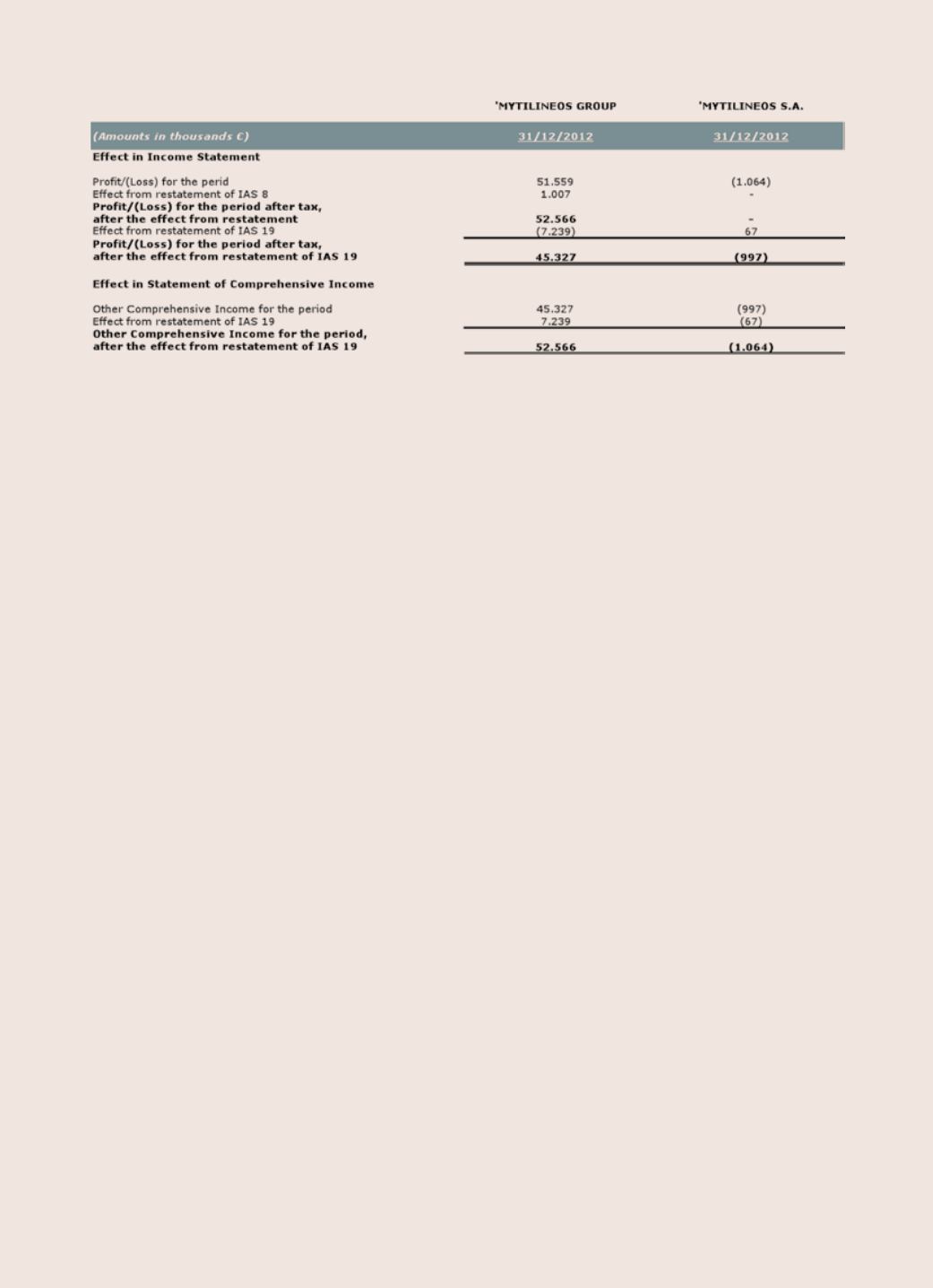

The application of the revised IAS 19 had an effect on the earnings per share for the year ended of 31st

December 2012.

• Accounting Policy Change for cost recognition «Electrolysis pots relining», of the subsidiary

Aluminium S.A.

In the financial year 2013, the Group changed the accounting policy for cost recognition «Electrolysis pots

relining», of the subsidiary Aluminium S.A. according to the relevant requirements of IAS 16:

An entity evaluates under this recognition principle all its property, plant and equipment costs at the time they

are incurred. These costs include costs incurred initially to acquire or construct an item of property, plant and

equipment and costs incurred subsequently to add to, replace part of, or service it.

Subsequent costs:

• Parts of some items of property, plant and equipment may require replacement at regular intervals. Items

of property, plant and equipment may also be acquired to make a less frequently recurring replacement.

Under the recognition principle in paragraph 7 IAS 16, an entity recognises in the carrying amount of an

item of property, plant and equipment the cost of replacing part of such an item when that cost is incurred

if the recognition criteria are met. The carrying amount of those parts that are replaced is derecognised in

accordance with the derecognition provisions of IAS 16.

• A condition of continuing to operate an item of property, plant and equipment may be performing regular

major inspections for faults regardless of whether parts of the item are replaced. When each major

inspection is performed, its cost is recognised in the carrying amount of the item of property, plant and

equipment as a replacement if the recognition criteria are satisfied. Any remaining carrying amount of the

cost of the previous inspection (as distinct from physical parts) is derecognised. This occurs regardless of

whether the cost of the previous inspection was identified in the transaction in which the itemwas acquired

or constructed. If necessary, the estimated cost of a future similar inspection may be used as an indication

of what the cost of the existing inspection component was when the item was acquired or constructed.

It is probable that future economic benefits associated with the item will flow to the entity; and the cost of the

item can be measured reliably.

The Group recognises in the carrying amount of an item of property, plant and equipment the relining cost